ISM Services Survey Weakens In August Amid "Highly Uncertain Path Ahead"

Tyler Durdan

After US manufacturing 'soft' surveys showed more progress in the V-shaped recovery, today's US Services data was expected to confirm that rebound.

- Markit US Manufacturing PMI 53.1 - best since Jan 2019

- ISM US Manufacturing 56.0 - best since Nov 2018

- Markit US Services PMI 55.0 (vs 54.7 exp) - best since March 2019

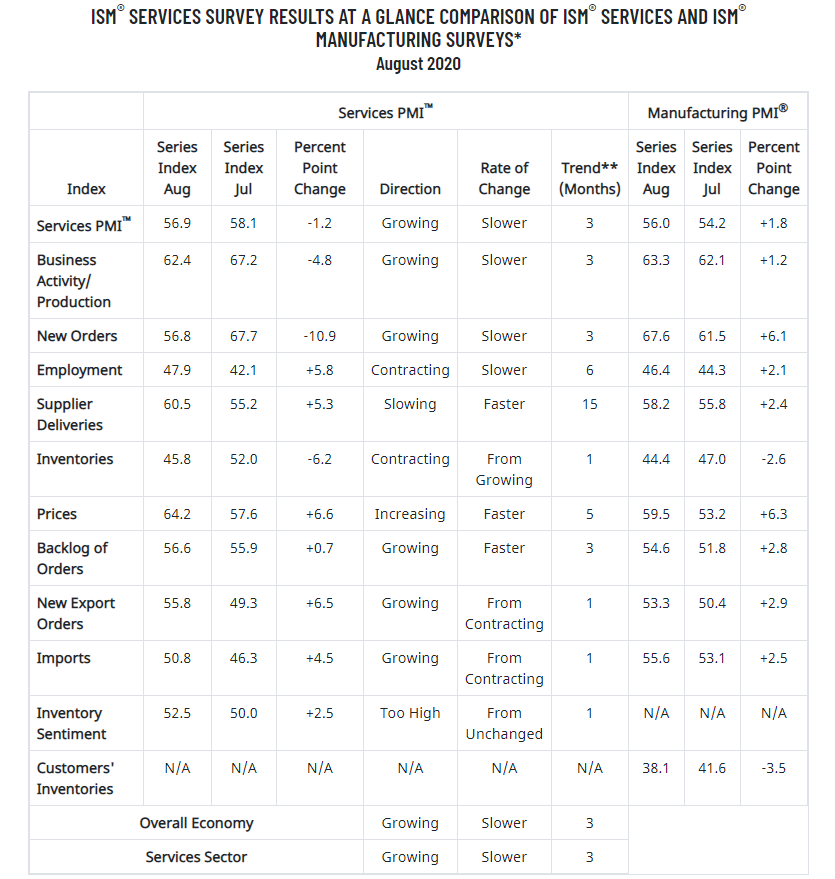

- ISM US Services 56.9 (vs 57.0 exp) - down from July's 58.1

So take your pick - ISM down, PMI up.

Source: Bloomberg

The Markit Services data was up from the flash print of 54.8 as both the Markit measures rose as the US Macro data overall has rolled over...

Source: Bloomberg

In the ISM Services sub-indices, we saw a notable weakening in new orders and activity.

ISM Service respondents were mixed:

“Our business activity is now thriving again, after modifications to our operations. While supply disruptions remain common, very critical items are more stable than in previous months. Tariff threats have caused more concern than in previous months due to actions in aluminum, and the rapid rise in lumber costs for construction expansions.” (Accommodation & Food Services)

“Overall, we are seeing improvement in the level of activity in the short term. Backlog of orders is inconsistent.” (Construction)

“Continuing pandemic uncertainties are challenging abilities to prepare for fall semester activities, resumption of in-person instruction and the research enterprise. Recent decision to provide all undergraduate instruction online has shifted priorities significantly, including reduced need for testing and increased need for remote teaching infrastructure.” (Educational Services)

“Revenue challenges for our customers still remain a primary challenge.” (Finance & Insurance)

“Clear signs of gearing up manufacturing and distribution for an extraordinary e-commerce Christmas. Brick-and-mortar likely closed to crowds. Also, hearing the other shoe is about to drop, probably in first quarter of 2021, on U.S.-China trade. “Get out of China now” is resonating.” (Information)

“We are significantly down from the pre-COVID-19 level. While month-over-month business activity is picking up, the pace is very slow and very slight.” (Wholesale Trade)

“Increase in service- and work-order requests are signs of economic improvement as companies reopen and begin to ramp up employment activity.” (Professional, Scientific & Technical Services)

What is notable is that whereas the Manufacturing New Orders series hit a 16 year high, the Services New Orders unexpectedly stumbled, resulting in one of the biggest deltas in the two New Orders series.

Putting all this together, the US composite index printed 54.6 in August, up from 50.3 at the start of the third quarter, to signal a strong upturn in business activity.

Sentiment about output over the coming year meanwhile edged down slightly from July’s 15-month high. Uncertainty surrounding the pandemic's future impact on the economy continued to weigh on confidence at manufacturers, contrasting with improved optimism among service providers.

“Surging inflows of new business helped propel service sector activity higher in August, with the sector growing at its fastest rate for almost one and a half years. Firms were often left struggling to meet demand and, despite taking on extra staff at a pace not seen for over six years, backlogs of uncompleted work accumulated at a rate exceeding anything recorded since 2009. The increase in backlogs of work bodes well for robust output growth to persist into September.

“Combined with the stronger picture emerging from manufacturing in August, the improved performance of the vast service sector adds to signs that the third quarter will see an impressive rebound in the economy from the collapse seen in the second quarter.

However, Williamson also notes that the survey also highlights how the rebound is very uneven and the recovery path remains highly uncertain.

“August’s growth was driven by financial and business services as well as tech firms, but consumer-facing sectors such as travel, tourism and recreation remained firmly in decline due to the need for ongoing social distancing.

“Companies across the board also remain concerned about resurgent virus infections and the durability of demand in the coming months after the initial rebound potentially fades, with uncertainty over the Presidential election adding further risks to the outlook for many companies.”

So something there for everyone - good news (but not enough to warrant any Fed pullback), bad news (but not enough to warrant any buy-stonks pullback)... all depends on which side of the boat you're on.

https://www.zerohedge.com/economics/ism-services-survey-weakens-august-amid-highly-uncertain-path-ahead